From the normally somewhat sane voice of Floyd Norris at the New York Times: Credit Crisis? Just Wait for a Replay.

What if it’s not just subprime?

Gee golly gosh, Floyd! I don't know.

Someone might actually have to do some investigative journalism on it. Who knows there may be all this data being analyzed on blogs and shit because there sure as teenage fuckery isn't any analysis in the MSM. And you might have to get off your ass and do some homework or something.

Friday, December 28, 2007

Thursday, December 27, 2007

Spread it!

Commercial paper is short-term (between 30 days and nine months.)

Commercial paper is short-term (between 30 days and nine months.)A2/P2 is lower-rated paper (as opposed to GE/Microsoft/Coke, etc.)

Fed can't do jack-motherfuckin'-shit about the spread unless they want to get into the commercial lending business themselves (and that would just about crash the dollar outright!) Please note the spread is far higher than 9/11!

We're dealing with a solvency crisis (hence, a confidence crisis.) Nobody wants to lend to anybody else because who knows where the bodies are buried?

Once again, for your sanity and mine, this is not a "liquidity crisis". The lack of liquidity is a symptom not a cause.

Tuesday, December 25, 2007

Spirit of the Season

"You're thinking of this bank all wrong. As if they had the money back in a safe. The money's not here. Your money's in a super senior synthetic tranche hedged with a CDS on Joe's house...right next to yours. Supported by the excess spread from the Kennedy house, and Mrs. Macklin's house, and a hundred others. Why, you're lending the Orange County's Firemens' Retirement Fund the money to short builders commercial paper, and then, they're all going to pay it back to you as best they can."

Monday, December 24, 2007

Holiday Cheer

From Reuters: One in Five Expect to Borrow to Heat Homes This Winter.

For perhaps as many as 27 million American adults, keeping warm this winter will mean borrowing money and 20 million will use credit cards to be able to afford their heating bills, according to a CreditCards.com poll.

Nearly 12 percent of Americans say they will need to borrow money to pay winter heating bills; 9 percent will need to use credit cards to be able to afford their heating bills.

Happy Holidays, everyone. Stay warm!

For perhaps as many as 27 million American adults, keeping warm this winter will mean borrowing money and 20 million will use credit cards to be able to afford their heating bills, according to a CreditCards.com poll.

Nearly 12 percent of Americans say they will need to borrow money to pay winter heating bills; 9 percent will need to use credit cards to be able to afford their heating bills.

Happy Holidays, everyone. Stay warm!

Sunday, December 23, 2007

Hooverville, here we come!

From Yahoo! News: Tent city in suburbs is cost of home crisis.

ONTARIO, California (Reuters) - Between railroad tracks and beneath the roar of departing planes sits "tent city," a terminus for homeless people. It is not, as might be expected, in a blighted city center, but in the once-booming suburbia of Southern California.

The noisy, dusty camp sprang up in July with 20 residents and now numbers 200 people, including several children, growing as this region east of Los Angeles has been hit by the U.S. housing crisis.

The unraveling of the region known as the Inland Empire reads like a 21st century version of "The Grapes of Wrath," John Steinbeck's novel about families driven from their lands by the Great Depression.

As more families throw in the towel and head to foreclosure here and across the nation, the social costs of collapse are adding up in the form of higher rates of homelessness, crime and even disease.

Maryanne Hernandez bought her dream house in San Bernardino in 2003 and now risks losing it after falling four months behind on mortgage payments.

"It's not just us. It's all over," said Hernandez, who lives in a neighborhood where most families are struggling to meet payments and many have lost their homes.

She has noticed an increase in crime since the foreclosures started. Her house was robbed, her kids' bikes were stolen and she worries about what type of message empty houses send.

But it is not just homeowners who are hit by the foreclosure wave. People who rent now find themselves in a tighter, more expensive market as demand rises from families who lost homes, said Jean Beil, senior vice president for programs and services at Catholic Charities USA.

"Folks who would have been in a house before are now in an apartment and folks that would have been in an apartment, now can't afford it," said Beil. "It has a trickle-down effect."

It's all good though. Hooray for downward mobility!

ONTARIO, California (Reuters) - Between railroad tracks and beneath the roar of departing planes sits "tent city," a terminus for homeless people. It is not, as might be expected, in a blighted city center, but in the once-booming suburbia of Southern California.

The noisy, dusty camp sprang up in July with 20 residents and now numbers 200 people, including several children, growing as this region east of Los Angeles has been hit by the U.S. housing crisis.

The unraveling of the region known as the Inland Empire reads like a 21st century version of "The Grapes of Wrath," John Steinbeck's novel about families driven from their lands by the Great Depression.

As more families throw in the towel and head to foreclosure here and across the nation, the social costs of collapse are adding up in the form of higher rates of homelessness, crime and even disease.

Maryanne Hernandez bought her dream house in San Bernardino in 2003 and now risks losing it after falling four months behind on mortgage payments.

"It's not just us. It's all over," said Hernandez, who lives in a neighborhood where most families are struggling to meet payments and many have lost their homes.

She has noticed an increase in crime since the foreclosures started. Her house was robbed, her kids' bikes were stolen and she worries about what type of message empty houses send.

But it is not just homeowners who are hit by the foreclosure wave. People who rent now find themselves in a tighter, more expensive market as demand rises from families who lost homes, said Jean Beil, senior vice president for programs and services at Catholic Charities USA.

"Folks who would have been in a house before are now in an apartment and folks that would have been in an apartment, now can't afford it," said Beil. "It has a trickle-down effect."

It's all good though. Hooray for downward mobility!

Friday, December 21, 2007

God Shave the Queen!

From the Times: London house price fall of 6.8% in past month stokes economy fears.

House prices in London have fallen by an average of £28,000 in the past month, as the capital sets the pace of an accelerating property downturn, a leading survey reports today.

Rightmove, the property website that tracks asking prices for homes across the market, says that prices tumbled by £20,000 a week in affluent Kensington and Chelsea – and by more than £10,000 a week in inner-city Hackney.

The company’s data shows that house prices fell by 3.2 per cent across the country, and by 6.8 per cent in London, over the month to the middle of December.

6.8% in a month is a fuckload of a fall, boys and girls.

I thought London was special. Prices never go down in Chelsea, Kensington and Wimbledon. While the Yanks were stupid enough to make sub-prime loans in Cleveland, they were the financially savvy ones, and because of that they were going to be the financial capital of the world (along with Dubai), and New York was in trouble, and the Brits were going to buy up most of Manhattan.

What happened instead, huh?

House prices in London have fallen by an average of £28,000 in the past month, as the capital sets the pace of an accelerating property downturn, a leading survey reports today.

Rightmove, the property website that tracks asking prices for homes across the market, says that prices tumbled by £20,000 a week in affluent Kensington and Chelsea – and by more than £10,000 a week in inner-city Hackney.

The company’s data shows that house prices fell by 3.2 per cent across the country, and by 6.8 per cent in London, over the month to the middle of December.

6.8% in a month is a fuckload of a fall, boys and girls.

I thought London was special. Prices never go down in Chelsea, Kensington and Wimbledon. While the Yanks were stupid enough to make sub-prime loans in Cleveland, they were the financially savvy ones, and because of that they were going to be the financial capital of the world (along with Dubai), and New York was in trouble, and the Brits were going to buy up most of Manhattan.

What happened instead, huh?

Spinning Jenny

The LA Times interviewed the Secretary of the Treasury, a Mr. Paulson: "These are not normal times".

Henry Paulson: The key is to get the balance right and not go so far that you cut off credit and make the situation worse. The Fed has also been looking at disclosure. I think when you look at the mortgage area, it's almost a caricature of what you see in other areas. You've got pages and pages of disclosure, which doesn't mean you're getting the people good information that they can understand. It's sort of, "Everybody cover their rear end," protect themselves legally. But, I've made the case several times, with all the disclosure there should be one simple page signed by the lender and the borrower that says, "Your monthly payment is x and it could be as high as y in a couple of years." The Fed I know has done some real consumer research on this.

Did the Fed do any research as to what happens when the consumer can't even afford the initial x? Or was that not part of the "real consumer research"?

I'm no lawyer but in that situation I don't think it's called "Disclosure". It's referred to as an "Adverse Action Notice".

Of course, that does run into the "cut off credit" part.

Back to the drawing board, Mr. Secretary!

Henry Paulson: The key is to get the balance right and not go so far that you cut off credit and make the situation worse. The Fed has also been looking at disclosure. I think when you look at the mortgage area, it's almost a caricature of what you see in other areas. You've got pages and pages of disclosure, which doesn't mean you're getting the people good information that they can understand. It's sort of, "Everybody cover their rear end," protect themselves legally. But, I've made the case several times, with all the disclosure there should be one simple page signed by the lender and the borrower that says, "Your monthly payment is x and it could be as high as y in a couple of years." The Fed I know has done some real consumer research on this.

Did the Fed do any research as to what happens when the consumer can't even afford the initial x? Or was that not part of the "real consumer research"?

I'm no lawyer but in that situation I don't think it's called "Disclosure". It's referred to as an "Adverse Action Notice".

Of course, that does run into the "cut off credit" part.

Back to the drawing board, Mr. Secretary!

Thursday, December 20, 2007

Jingle Mail, Jingle Mail, Jingle All the Way...

From the Wall Street Journal: Now, Even Borrowers With Good Credit Pose Risks.

Kenneth Lewis acted far ahead of the competition in 2001, when he got Bank of America out of the business of issuing subprime mortgages. While profit margins on these loans to risky borrowers seemed tempting, the bank's chief executive believed the default risks were too hefty to justify.

So what is Mr. Lewis worrying about today? In an interview last week with Wall Street Journal editors, he expressed concern that even borrowers with strong credit scores might turn out to be default risks if housing prices keep tumbling. In other words, what is being portrayed as a credit-quality problem with the riskiest 20% of the mortgage market could spread to a much wider cross-section of home loans.

"There's been a change in social attitudes toward default," Mr. Lewis says. Bankers typically have believed that cash-strapped borrowers would fall behind on their credit cards, car payments and other debts -- but would regard mortgage defaults as calamities to be avoided at all costs. That isn't always so anymore, he says.

"We're seeing people who are current on their credit cards but are defaulting on their mortgages," Mr. Lewis says. "I'm astonished that people would walk away from their homes." The clear implication: At least a few cash-strapped borrowers now believe bailing out on a house is one of the easier ways to get their finances back under control.

Such behavior was highlighted in a page-one Journal article this week about the housing quagmire in Corona, Calif. One couple bought a home for $557,000 in 2004 and then refinanced it for increasing amounts as property prices soared, eventually ending up with an $835,000 mortgage -- and extra cash for personal expenses. The couple then bought a cheaper home in Texas and stopped making payments on the Corona home in June. As the countdown to foreclosure continues, it looks increasingly likely lenders will be stuck with that house.

First off, from a rational economic point of view, mailing back the key is absolutely the "correct" thing to do. It is somebody else's problem; in this case, the MBS holder's. They took on the risk, loaned these people the money. If it didn't work out, so sad, too bad...

Secondly, doesn't Mr. Lewis realize that value is perceived by how much effort it takes to achieve something? How useful is "good credit" when any fool gets two to three credit card offers two weeks out of bankruptcy?

By comparison, a "renter" has to all but subject him/herself to an anal probe. In most places, they have to get a credit check, two letters of reference, put up a deposit in escrow, and pay the first month's rent.

If people have no skin in the game, they will walk away. One doesn't have to be Warren Buffett to figure this one out.

The blunt truth is any mortgage product that didn't involve a hefty downpayment is doomed to fail. Period. It's all about skin in the game. No amount of tap dancing around this subject will work.

Lastly, it is critical to keep in mind the role of psychology in these things. If it becomes socially acceptable to go to a party and say, "I mailed in the keys to the bank. Hah hah hah!", the banks are doomed. Flat out, doomed. There's not a power in the world (including the central banks) that can rescue them. Social acceptibility is the ultimate arbiter of many a behavior, and if everyone's doing it, there's no stigma attached to it.

(And just for the record, I'm willing to bet that this is the scenario that will come to pass. Why? It was socially acceptable in the early-to-mid-90's, and it will be again.)

Incidentally, that story up there was in yesterday's Journal. The couple pulled out the "phantom equity", bought a brand new Lexus and a SUV, and a house in Texas (most probably in cash.)

Why?

You can't go after a house in Texas in bankruptcy, and you certainly can't go after a fully-paid one. You also can't go after a car (because a car is considered the modern equivalent of a "horse" which cannot be repossessed in Texas!) The lender is pretty much screwed. This particular couple has played the system like a Stradivarius.

Welcome to Planet Reality(TM), Mr. Lewis. We hope you will enjoy your stay.

Kenneth Lewis acted far ahead of the competition in 2001, when he got Bank of America out of the business of issuing subprime mortgages. While profit margins on these loans to risky borrowers seemed tempting, the bank's chief executive believed the default risks were too hefty to justify.

So what is Mr. Lewis worrying about today? In an interview last week with Wall Street Journal editors, he expressed concern that even borrowers with strong credit scores might turn out to be default risks if housing prices keep tumbling. In other words, what is being portrayed as a credit-quality problem with the riskiest 20% of the mortgage market could spread to a much wider cross-section of home loans.

"There's been a change in social attitudes toward default," Mr. Lewis says. Bankers typically have believed that cash-strapped borrowers would fall behind on their credit cards, car payments and other debts -- but would regard mortgage defaults as calamities to be avoided at all costs. That isn't always so anymore, he says.

"We're seeing people who are current on their credit cards but are defaulting on their mortgages," Mr. Lewis says. "I'm astonished that people would walk away from their homes." The clear implication: At least a few cash-strapped borrowers now believe bailing out on a house is one of the easier ways to get their finances back under control.

Such behavior was highlighted in a page-one Journal article this week about the housing quagmire in Corona, Calif. One couple bought a home for $557,000 in 2004 and then refinanced it for increasing amounts as property prices soared, eventually ending up with an $835,000 mortgage -- and extra cash for personal expenses. The couple then bought a cheaper home in Texas and stopped making payments on the Corona home in June. As the countdown to foreclosure continues, it looks increasingly likely lenders will be stuck with that house.

First off, from a rational economic point of view, mailing back the key is absolutely the "correct" thing to do. It is somebody else's problem; in this case, the MBS holder's. They took on the risk, loaned these people the money. If it didn't work out, so sad, too bad...

Secondly, doesn't Mr. Lewis realize that value is perceived by how much effort it takes to achieve something? How useful is "good credit" when any fool gets two to three credit card offers two weeks out of bankruptcy?

By comparison, a "renter" has to all but subject him/herself to an anal probe. In most places, they have to get a credit check, two letters of reference, put up a deposit in escrow, and pay the first month's rent.

If people have no skin in the game, they will walk away. One doesn't have to be Warren Buffett to figure this one out.

The blunt truth is any mortgage product that didn't involve a hefty downpayment is doomed to fail. Period. It's all about skin in the game. No amount of tap dancing around this subject will work.

Lastly, it is critical to keep in mind the role of psychology in these things. If it becomes socially acceptable to go to a party and say, "I mailed in the keys to the bank. Hah hah hah!", the banks are doomed. Flat out, doomed. There's not a power in the world (including the central banks) that can rescue them. Social acceptibility is the ultimate arbiter of many a behavior, and if everyone's doing it, there's no stigma attached to it.

(And just for the record, I'm willing to bet that this is the scenario that will come to pass. Why? It was socially acceptable in the early-to-mid-90's, and it will be again.)

Incidentally, that story up there was in yesterday's Journal. The couple pulled out the "phantom equity", bought a brand new Lexus and a SUV, and a house in Texas (most probably in cash.)

Why?

You can't go after a house in Texas in bankruptcy, and you certainly can't go after a fully-paid one. You also can't go after a car (because a car is considered the modern equivalent of a "horse" which cannot be repossessed in Texas!) The lender is pretty much screwed. This particular couple has played the system like a Stradivarius.

Welcome to Planet Reality(TM), Mr. Lewis. We hope you will enjoy your stay.

Wednesday, December 19, 2007

"Build it, they will come"

From the Tampa Tribune: Empty Storefronts Filled With Hope And Promise.

Although Channelside Drive, the Arts District and the Franklin Street corridor have begun to show some retail stirrings after years of stagnation and promises, few would agree that downtown Tampa has yet to show its potential as a vibrant urban center for shopping, dining and entertainment.

Retail expert Lee Nelson, a senior associate at CB Richard Ellis in Tampa, said restaurants and shops will "flock" to the newly built space. But it will take years - not months - for the vacancies to be filled.

"Retailers have to have customers," she said. "Until those condos are full of people, the retail will not come. Then it will be vibrant and exciting."

Yes, "then" it will be vibrant and exciting. Meanwhile, you expect the people to come there on what exactly? Faith?

New York's Fifth Avenue, London's Oxford Street and Chicago's Magnificent Mile have nothing to fear from downtown Tampa.

I would think not! Has this guy ever even walked down either of the three? Places like these don't just arise overnight, and they sure as hell don't arise due to some "marketing plan".

Same goes for all the cities planning "art districts". You can't plan these things!

Enjoy the Section 8 in a few years!

Although Channelside Drive, the Arts District and the Franklin Street corridor have begun to show some retail stirrings after years of stagnation and promises, few would agree that downtown Tampa has yet to show its potential as a vibrant urban center for shopping, dining and entertainment.

Retail expert Lee Nelson, a senior associate at CB Richard Ellis in Tampa, said restaurants and shops will "flock" to the newly built space. But it will take years - not months - for the vacancies to be filled.

"Retailers have to have customers," she said. "Until those condos are full of people, the retail will not come. Then it will be vibrant and exciting."

Yes, "then" it will be vibrant and exciting. Meanwhile, you expect the people to come there on what exactly? Faith?

New York's Fifth Avenue, London's Oxford Street and Chicago's Magnificent Mile have nothing to fear from downtown Tampa.

I would think not! Has this guy ever even walked down either of the three? Places like these don't just arise overnight, and they sure as hell don't arise due to some "marketing plan".

Same goes for all the cities planning "art districts". You can't plan these things!

Enjoy the Section 8 in a few years!

Tuesday, December 18, 2007

Sheer Brilliance

From the Boston Herald: Realtors face tough reality.

“If sales are down, revenue is down,” said Ruth Pino, a Carlson GMAC branch executive in Gloucester.

Quick! Nobel Committee, give this woman the Prize!

“If sales are down, revenue is down,” said Ruth Pino, a Carlson GMAC branch executive in Gloucester.

Quick! Nobel Committee, give this woman the Prize!

Comment puis-je dire?

From the Lower Hudson online: Lots of blame to go around in subprime mortgage crisis.

For months Marie Chantale Joseph and her husband, Daniel, have been unsuccessfully trying to refinance their home before their interest rate spikes in April.

Already, Daniel, a taxi driver, is working 18 hours a day and on weekends to pay the approximately $4,800 a month they owe, and Marie, a babysitter, works as many hours as she can.

"In my country it is different. No one can come and take your home away from you," said Marie Chantale, who must pay about $8,000 a month beginning in April, or lose her home to foreclosure. "Here, if they know you don't know what you are doing, they take advantage of you."

Firstly, the idea that Haiti is more ethical than the US is absurd. We're talking about literally the poorest nation in the Western Hemisphere which also has the dubious distinction of being a failed state.

Secondly, we're talking about a baby-sitter and a cab-driver buying a $500,000 house with monthly payments of $8,000.

Let me repeat that for emphasis: a baby-sitter and a cab-driver with $8,000 monthly payments. (That's $96,000 a year for 30 years, or roughly $3 million!)

Here's the "much esteemed" Federal Reserve's Survey of Consumer Finances, (PDF link) where you can figure out for yourself that even a family in the top 5% of incomes cannot possibly make those payments. They would literally be scraping by, and hope to God and cross their hearts that nothing goes wrong.

Ponder that! No fuckups for 30 straight years -- no medical problems, no unexpected expenses, no recessions, no layoffs, absolute perfection for 30 years.

What is easier to believe?

That they had no clue of what they were doing, or they were gaming the system, and after the shit hits the fan, they fuck off back to Haiti?

You can decide that for yourself!

For months Marie Chantale Joseph and her husband, Daniel, have been unsuccessfully trying to refinance their home before their interest rate spikes in April.

Already, Daniel, a taxi driver, is working 18 hours a day and on weekends to pay the approximately $4,800 a month they owe, and Marie, a babysitter, works as many hours as she can.

"In my country it is different. No one can come and take your home away from you," said Marie Chantale, who must pay about $8,000 a month beginning in April, or lose her home to foreclosure. "Here, if they know you don't know what you are doing, they take advantage of you."

Firstly, the idea that Haiti is more ethical than the US is absurd. We're talking about literally the poorest nation in the Western Hemisphere which also has the dubious distinction of being a failed state.

Secondly, we're talking about a baby-sitter and a cab-driver buying a $500,000 house with monthly payments of $8,000.

Let me repeat that for emphasis: a baby-sitter and a cab-driver with $8,000 monthly payments. (That's $96,000 a year for 30 years, or roughly $3 million!)

Here's the "much esteemed" Federal Reserve's Survey of Consumer Finances, (PDF link) where you can figure out for yourself that even a family in the top 5% of incomes cannot possibly make those payments. They would literally be scraping by, and hope to God and cross their hearts that nothing goes wrong.

Ponder that! No fuckups for 30 straight years -- no medical problems, no unexpected expenses, no recessions, no layoffs, absolute perfection for 30 years.

What is easier to believe?

That they had no clue of what they were doing, or they were gaming the system, and after the shit hits the fan, they fuck off back to Haiti?

You can decide that for yourself!

Monday, December 17, 2007

Liquidity v/s Solvency

We seem to be hearing a lot about the "liquidity crisis". However, this is fundamentally a "solvency crisis".

Here's the situation in a nutshell:

Money was loaned in copious quantities on the basis of highly inflated appraisals of questionable collateral. Then the system leveraged the motherfuckin'-crap (to use a technical term) out of an already highly leveraged position. The money was spent and is not coming back.

Please show me how "printing money" can reverse anything.

Let's review the above in terms that we can all understand:

You sell cars. I buy two with counterfeit cash. Your suppliers balk and refuse to replenish your inventory. Meanwhile, I've sold the cars, and blown the money on booze and hookers.

What are you gonna do? Possibly have me arrested but you're still out the cars and the cash.

Now add the above stated leverage, and you will see the problem.

Here's the situation in a nutshell:

Money was loaned in copious quantities on the basis of highly inflated appraisals of questionable collateral. Then the system leveraged the motherfuckin'-crap (to use a technical term) out of an already highly leveraged position. The money was spent and is not coming back.

Please show me how "printing money" can reverse anything.

Let's review the above in terms that we can all understand:

You sell cars. I buy two with counterfeit cash. Your suppliers balk and refuse to replenish your inventory. Meanwhile, I've sold the cars, and blown the money on booze and hookers.

What are you gonna do? Possibly have me arrested but you're still out the cars and the cash.

Now add the above stated leverage, and you will see the problem.

Thursday, December 13, 2007

Have you heard of ...

... Bankhaus Herstatt?

You will, kids, you will. This is like déjà vu, all over again!

You will, kids, you will. This is like déjà vu, all over again!

Monday, December 10, 2007

Swiss Cheese

Once again, the Wall Street Journal reports: UBS Gains Two New Investors, Writes Down $10 Billion.

UBS AG Monday said that two strategic foreign investors committed to inject capital worth 13 billion Swiss francs ($11.5 billion) as part of a broader move to strengthen capital as the Swiss bank announced a further $10 billion in write-downs on subprime holdings.

The bank said it was now possible that it will record a net loss for the full year.

UBS is issuing mandatory convertible notes worth 13 billion francs for these investments, which will pay a coupon of 9%.

Beyond the investments from these two parties, UBS plans to sell treasury shares and replace its 2007 cash dividend with a stock dividend, boosting capital by 6.4 billion francs.

9% while 3-month Treasuries are barely yielding 3%!

That's like going down the pawn-shop to borrow from Fat Tony.

And a stock dividend is less than worthless.

Before the stock dividend, each investor owns a certain fraction of the company. After the dividend, ta-daa, they own the same fraction.

It's like your mom cutting a cake into two pieces, and saying, "Now you have double the cake."

Watch out,suckers er, UBS investors!

UBS AG Monday said that two strategic foreign investors committed to inject capital worth 13 billion Swiss francs ($11.5 billion) as part of a broader move to strengthen capital as the Swiss bank announced a further $10 billion in write-downs on subprime holdings.

The bank said it was now possible that it will record a net loss for the full year.

UBS is issuing mandatory convertible notes worth 13 billion francs for these investments, which will pay a coupon of 9%.

Beyond the investments from these two parties, UBS plans to sell treasury shares and replace its 2007 cash dividend with a stock dividend, boosting capital by 6.4 billion francs.

9% while 3-month Treasuries are barely yielding 3%!

That's like going down the pawn-shop to borrow from Fat Tony.

And a stock dividend is less than worthless.

Before the stock dividend, each investor owns a certain fraction of the company. After the dividend, ta-daa, they own the same fraction.

It's like your mom cutting a cake into two pieces, and saying, "Now you have double the cake."

Watch out,

Saturday, December 08, 2007

Dow (Corning) Deflation

Well, the Wall Street Journal has done it again: Evidence Grows That Consumers Are Pulling Back.

The latest sign that growth in consumer spending, the mainstay of the U.S. economy, is slowing? A nip and tuck in spending on cosmetic surgery.

The slowdown was a hot topic at the meeting of the American Society of Plastic Surgeons in Baltimore this fall. One breast-implant maker sees hints of a slowdown in demand.

Well, looks like Bubbles and Jiggles are going to go down after all (and not that way either, you perverts!)

And who needs AAA-rated bonds when you have double-D's?

Russ Meyer, come back. America needs you!

The latest sign that growth in consumer spending, the mainstay of the U.S. economy, is slowing? A nip and tuck in spending on cosmetic surgery.

The slowdown was a hot topic at the meeting of the American Society of Plastic Surgeons in Baltimore this fall. One breast-implant maker sees hints of a slowdown in demand.

Well, looks like Bubbles and Jiggles are going to go down after all (and not that way either, you perverts!)

And who needs AAA-rated bonds when you have double-D's?

Russ Meyer, come back. America needs you!

Tuesday, December 04, 2007

House Prices and Foreclosures

(Source: Boston Fed.)

This is data just for Massachussetts.

There are two ways to interpret this graph:

The rise in prices predicts foreclosures. It suggests that people bought houses they couldn't really afford on their incomes.

The second is that if you look at prices, they didn't hit the 0% growth mark until after foreclosures had taken off. That suggests that people were buying houses with the implicit assumption of rising prices.

Both, of course, are familiar to people who have been following this mania.

Saturday, December 01, 2007

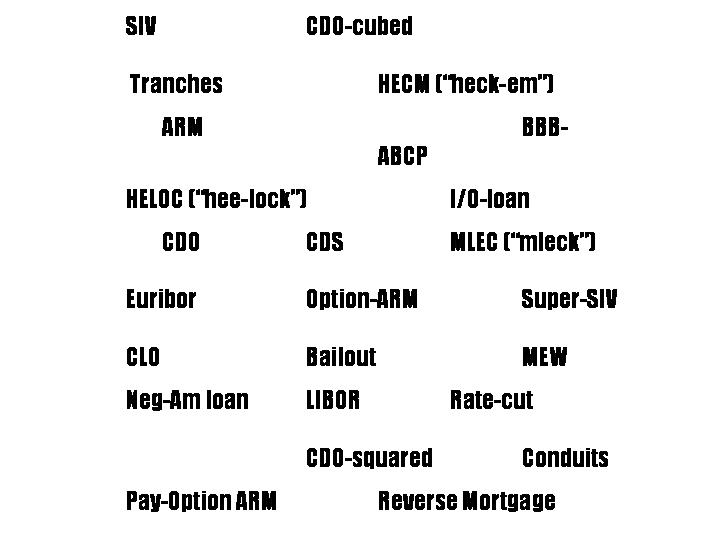

Beer Bingo

Truly a venerable tradition if ever there was one!

Truly a venerable tradition if ever there was one!The rules are simple.

You have to swill one gulp of beer each time one of the words in the above Alphabet Soup is mentioned in the press. If you don't know what the word means, and you admit it, you have to take three gulps. If challenged to explain, and you fail, you must down what's left in the glass.

Of course, this will mean that you will frequently be liquored up before breakfast but that's probably the only reasonable way to deal with the bollix-ed cock-up clusterfuck that is the US Economy.

Subscribe to:

Posts (Atom)